How the WIPP pension actually works

Ask three senior members how the pension works and you'll get three different answers. None of them lying. All of them partly right. Most guys never see the actual mechanics laid out in one place, so they guess at where they stand on the Rule of 90 and hope payroll and the pension office have it handled. You can do better than hope. DockBook tracks your pension credits and your Rule of 90 progress off the shifts you already log, so you can see the number instead of guessing it. But first, here is how the pension actually works.

The WIPP is the defined-benefit pension that covers BCMEA / ILWU Canada longshoremen. It's a multi-employer plan and has been since 1998. Every year you work, you build up service. Every year of service translates into a fixed monthly benefit at retirement. Your pension is not tied to the stock market. It's tied to the contract.

That last part is the part most guys miss. Your WIPP pension goes up when the negotiated benefit rate goes up, not when the TSX has a good year.

Who's covered

Two groups are members of the WIPP:

- Active union members. If you're a member of ILWU Canada, you're in.

- A-Board Welfare Casuals. Effective April 1, 2014, casuals who reach A-Board Welfare status became members of the plan. If you become an A-Board Welfare Casual on or before January 31 of a given year, your membership backdates to January 1 of that year.

Casuals below A-Board Welfare are not yet plan members, but their service can still count later (more on that below).

How a year of credited service is earned

This is where most of the confusion lives. The rule changed in 2016, so older guys learned one set of rules and newer guys are working under another.

Pre-2016 rule: the 800-hour test

Before January 1, 2016, you got a full year of credited service for any year in which you worked at least 800 hours. Less than 800 and you got partial credit (between January 1, 1989 and December 31, 2015). Effectively if you weren't getting steady work, you weren't building full pension years.

Post-2015 rule: the annual earnings limit

Starting January 1, 2016, the test stopped being hours and became earnings. To get a full year of credited service, you have to earn at least the annual earnings limit:

| Year | Annual earnings limit |

|---|---|

| 2024 | $108,000 |

| 2025 | $114,000 |

| 2026 | $120,000 |

Earn less than the limit, you get partial credit. Earn under 25% of the limit, your service for that year may be frozen (your accrued benefit stays put at the rates in effect that year, no further growth from that year's service). The 25% floor in 2026 works out to $30,000.

This is a real risk for casuals working under-utilised years and for senior members who pull back hours in their late career. If you're chasing a year of credited service, the relevant target now is the dollar figure, not 800 hours.

How casual service folds in

Casual service used to be invisible until you joined the union. After 2016, casual service can be counted retroactively for years where you earned at least a percentage of the annual earnings limit. The percentage has stepped down over time:

| Effective date | Casual earnings requirement |

|---|---|

| January 1, 2016 | 75% of annual earnings limit |

| January 1, 2017 | 50% of annual earnings limit |

| January 1, 2025 | 25% of annual earnings limit |

The catch: this credit is only granted once you become a union member. The casual years themselves can be retroactively counted, but only after you've made the union. If you spend five years casualling and earn over the threshold each year, those five years get added to your credited service once you become a member. If you never make the union, those years don't count toward your pension.

This is the single biggest reason to track your earnings as a casual. The years you're underpaid relative to the threshold are years you don't get back.

How much is the monthly benefit

The WIPP is a defined-benefit plan, which means your retirement income is calculated by a fixed formula:

Monthly pension at age 65 = Benefit Rate × Years of Credited Service

The benefit rate is set by the trustees and goes up over time as the plan negotiates increases. Recent rates:

| Year | Benefit Rate (per month, per year of service) |

|---|---|

| 2024 | $180.00 |

| 2025 | $190.00 |

| 2026 | $200.00 |

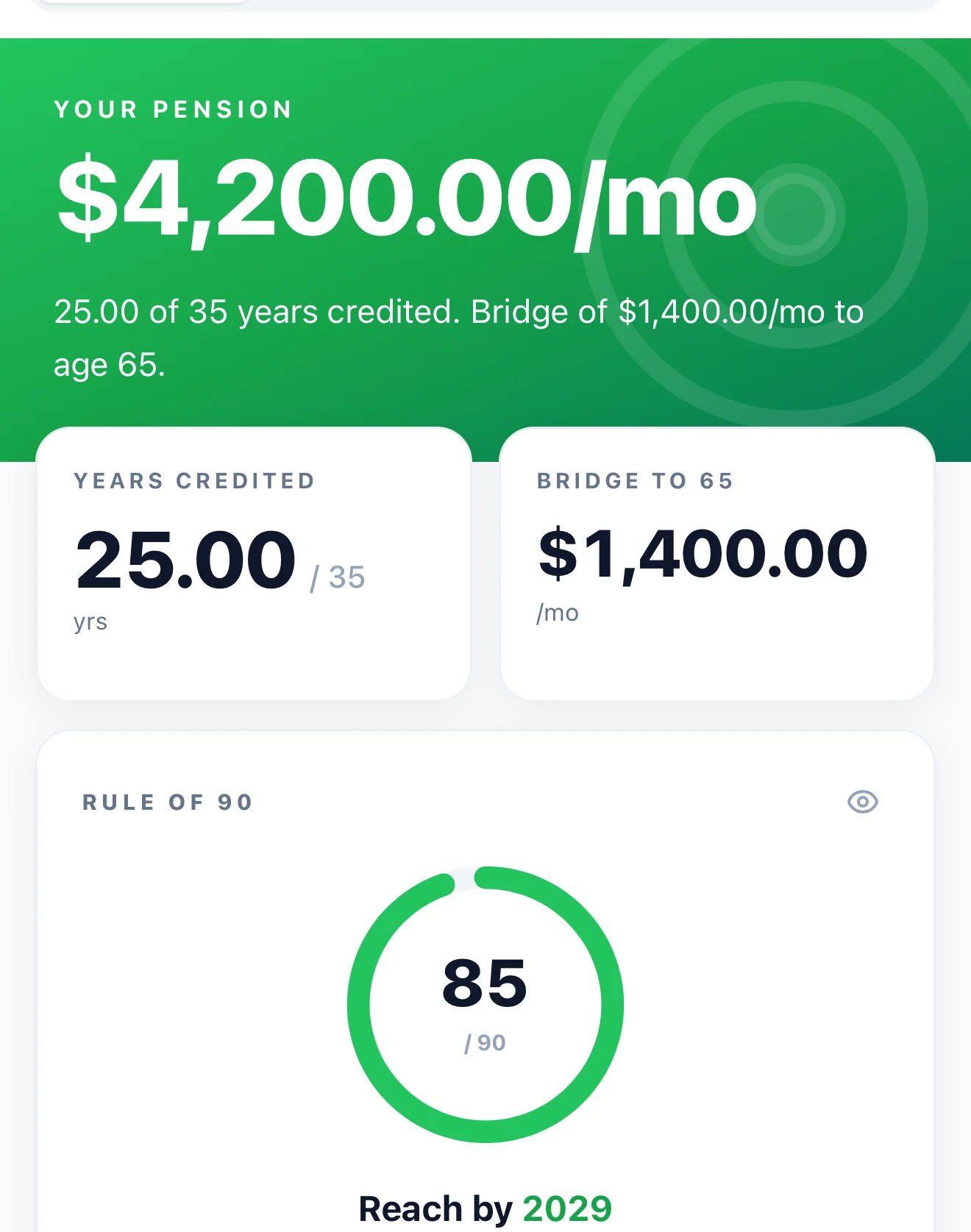

So a member with 25 years of credited service retiring at age 65 in 2026 would receive $200 × 25 = $5,000 per month as a basic pension at normal retirement.

The maximum credited service caps at 35 years. After that, you keep working but you don't keep building pension. A 35-year career at the 2026 rate locks in $200 × 35 = $7,000 per month basic, before any bridge benefit.

Pensioners already drawing the WIPP also got a +1.9% increase on January 1, 2026, indexed to Vancouver CPI (Sep 2024 to Sep 2025).

When you can retire

There are three retirement paths:

Normal Retirement (age 65)

Your normal retirement date is the first day of the month after you turn 65. You can keep working past 65 and keep accruing service (up to the 35-year cap), but you have to start collecting your pension by the end of the calendar year you turn 71. That's a CRA rule, not a plan rule, but the plan enforces it.

Regular Early Retirement (age 55, reduced)

You can retire as early as age 55 with at least 2 years of Waterfront Service. The catch: your pension is reduced by approximately 6% per year for every year you retire before normal retirement age (65). The plan doesn't spell out whether that reduction is simple or compounded, so don't trust a back-of-envelope estimate for your specific case. Ask the pension administrator. They can tell you exactly what the reduction works out to for your age and service.

Special Early Retirement: the Rule of 90

This is the one most members are aiming for. You qualify for Special Early Retirement with no reduction if either:

- You're at least age 60 with at least 25 years of credited service, OR

- You're at least age 55 and your age plus credited service equals 90 or more.

Plus you need at least 2 years of credited service in the 36 months immediately before applying.

Effective January 1, 2023, there is no reduction to the basic pension at Special Early Retirement. Before that date there was a reduction. If you've been told the Rule of 90 still has a haircut, that information is out of date.

The math: a member who started at 25 and built 30 years of service is 55 with 30 years credited. 55 + 30 = 85. Doesn't qualify. Wait three more years: 58 with 33 years credited. 58 + 33 = 91. Qualifies.

If you're wondering how close you are to the Rule of 90, DockBook tracks it for you. It counts your credited years off your logged shifts and lets you fill in the years you worked before you started using the app, so your Rule of 90 progress stays current as you work. See the full pension tracker on DockBook for BCMEA, or run a quick number on the free pay calculator.

The Bridge Benefit

This is the part that's separate from your basic pension. The Bridge Benefit is a top-up paid only between your retirement date and age 65, designed to bridge the gap before CPP and OAS start.

The rate has been $36.35 per month, per year of service since January 1, 2010. The cap was 25 years at that time, then raised to 35 years effective January 1, 2017.

Maximum bridge: $36.35 × 35 = $1,272.25 per month, paid until you turn 65, then it stops. So if you retire at 58 with 30 years of service, your bridge is $36.35 × 30 = $1,090.50 per month for 7 years (58 to 65), on top of your basic pension. Then at 65, the bridge cuts off and your basic pension continues for life.

Vesting and contributions

You contribute 3% of covered earnings by payroll deduction (effective April 1, 2014). The cap moves with the annual earnings limit, so:

| Year | Earnings cap | Max employee contribution |

|---|---|---|

| 2024 | $108,000 | $3,240 |

| 2025 | $114,000 | $3,420 |

| 2026 | $120,000 | $3,600 |

For terminations after June 30, 2011, vesting is full. Whatever credited service you've earned, you keep, even if you leave the industry. You apply for it later as a deferred vested pension.

Reinstatement

If you leave the industry and come back, your prior service can be reinstated provided three conditions:

- You return to work within 36 months of your last credited hours, AND

- You earn at least 0.25 years of credited service in each calendar year after returning, AND

- You complete at least two years of credited service in any three consecutive calendar years after returning.

Miss any of those and the reinstatement isn't automatic.

The RRSP contribution room hit

This is the one most members don't realise until tax time. Because the WIPP is a defined-benefit pension, the CRA applies a Pension Adjustment (PA) to your T4 every year. The PA reduces the RRSP contribution room you'd otherwise have.

| Year | PA per year of credited service |

|---|---|

| 2024 | $18,840 |

| 2025 | $19,920 |

| 2026 | $21,000 |

So if you got a full year of credited service in 2025, your RRSP room for the following year is reduced by $19,920. A full 2026 year reduces it by $21,000. For a member earning the cap and getting full credit, that's most or all of the RRSP room they'd otherwise have generated.

That's not a bug. The PA mechanism is how CRA equalises tax-deferred retirement savings between people in DB pension plans and people without one. But it does mean that aggressive RRSP contributions on top of full WIPP service can push you into over-contribution territory if you don't watch the numbers.

The practical takeaway: the WIPP is doing the heavy lifting on your retirement savings already. Your CRA Notice of Assessment shows your remaining RRSP room each year. For specific advice on what to do with whatever room you have, talk to a registered financial advisor who knows DB pension plans.

What about Past Service Pension Adjustments

PSPAs come up in two situations:

- The plan is given a benefit increase that applies retroactively to past years of service and exceeds the increase in the Average Industrial Wage. That generates a PSPA, which further reduces your RRSP room.

- A new union member is credited with casual service after 1997. That triggers a PSPA on the casual years.

For most members, PSPAs are infrequent. They only really matter if you're already maxing your RRSP room because they can cause unintended over-contribution.

If you're about to become a Union Member, read this first

This is the scenario where PSPA actually bites and the post-2016 casual-service rules collide with CRA limits. Worth the extra paragraphs.

When you go from Casual to Union Member, all your post-1997 credited casual years vest into WIPP at once. Each of those years attracts a Past Service Pension Adjustment at the year-of-joining PA rate. At the 2026 PA of $21,000, six pensionable casual years means a PSPA of $126,000. CRA requires you to have enough unused RRSP contribution room to absorb that PSPA. Without enough room, the recognition can't fully happen.

CRA gives you two paths if your cumulative unused RRSP room can't absorb the PSPA:

- Forfeit some or all of the casual service. Those casual years simply aren't recognized. They drop off your credited-service total. You keep the union membership, you lose the casual pension years.

- Make a qualifying RRSP withdrawal to create room. Important: spousal RRSP withdrawals do not qualify for this purpose.

This is strictly between you and CRA. The Plan Administrator doesn't handle the RRSP side.

Practical sequence the trustees recommend:

- Before attaining union membership, pull your most recent CRA Notice of Assessment and check your available RRSP contribution room.

- If your room is insufficient, don't contribute to your RRSP (or your spouse's RRSP) in the years leading up to joining. That contribution room is what will absorb the PSPA when you join. Burning it now means giving up casual years later.

- Talk to a financial planner who has handled DB-plan PSPAs. Not all of them have. The pension office can clarify the WIPP-side mechanics but won't give RRSP advice.

- If your room is insufficient at first, you may be able to reapply later once more room becomes available. Not guaranteed, but possible.

If you want to talk to the pension office directly, the contacts are:

- Email: pensions@webc.ca

- Phone: 604-689-7184, extension 6

- Office: the WEBC office (same one that handles welfare)

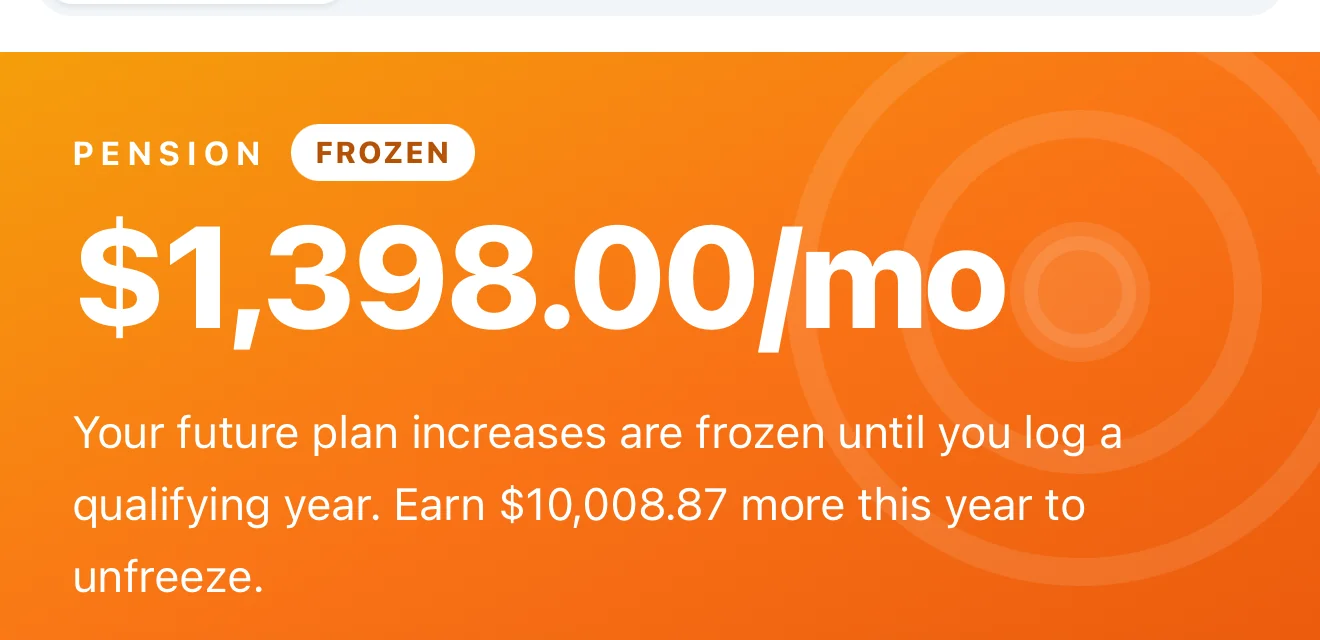

Frozen benefits

This is one rule that's been in place since January 1, 1997. The threshold for triggering it changed when the credited-service test moved from hours to earnings in 2016.

If you fall below the threshold in a given year, your Basic and Bridge pensions earned to date get frozen at the benefit rates in effect that year:

- From January 1, 1997 through December 31, 2015: triggered if you accrued less than 200 credited hours.

- From January 1, 2016 onward: triggered if you accrued less than 0.25 years of credited service (earnings under 25% of the annual earnings limit).

Frozen doesn't mean lost. It means that portion of your pension stops growing with future benefit-rate increases. Your existing accrued benefit is protected at the rate in effect when the freeze hit. Service in subsequent years (above the threshold) continues to grow normally at the prevailing rate.

What DockBook does with all this

DockBook's Retirement Plan section applies these rules to your logged shifts. It tracks Rule of 90 eligibility, your pension credits per year, your work history, and the M&M allowance. If you worked years before you started using DockBook, you can manually enter that history and it'll fold into the projection.

That's the whole point. The pension rules above are the kind of thing you check once and then forget the details of, right up until you're a few years out from retiring and trying to work out whether you've hit the Rule of 90 yet. DockBook keeps the running count for you so the answer is already there when you need it. See the full pension tracker on DockBook for BCMEA, or run a quick number now on the free pay calculator.

For another BCMEA rule that's easy to get wrong, see how stat holiday pay actually works.

Caveats

This is a plain-English explainer based on the current WIPP plan documents, updated with the 2026 numbers. It is not a legal document, not financial advice, and not a substitute for the actual plan text or a conversation with the plan administrator. Numbers (benefit rate, earnings limit, PA, etc.) are accurate as of the date posted but the plan trustees update them periodically. Always verify the current numbers with the WIPP administrator before making a retirement decision.

If you spot something that's out of date or wrong, email me. I update these posts as the plan changes.

Frequently asked

What is the Rule of 90?

You can take Special Early Retirement with no reduction to your basic pension once your age plus your years of credited service total 90, provided you are at least 55 and have 2 years of credited service in the 36 months before applying. Since January 1, 2023 there is no reduction at this milestone.

How much is the WIPP pension worth per year of service?

The 2026 benefit rate is $200 per month for each year of credited service, paid from age 65. Your basic pension is that rate times your years of credited service, capped at 35 years.

How do I earn a year of credited service?

Since 2016 it is based on earnings, not hours. You need to earn at least the annual earnings limit ($120,000 in 2026) for a full year. Earn less and you get partial credit; earn under 25% of the limit ($30,000) and that year's service can be frozen.

What is the Bridge Benefit?

A top-up paid only between your retirement date and age 65, at $36.35 per month for each year of service, capped at 35 years. It bridges the gap before CPP and OAS begin, then stops at 65.

Does the WIPP reduce my RRSP room?

Yes. Because it is a defined-benefit plan, the CRA applies a Pension Adjustment to your T4 each year ($21,000 for a full 2026 year), which lowers the RRSP contribution room you would otherwise have.

Have a question about this post or spot something to fix? Email me directly.