How the PMA Pay Guarantee Plan actually works

The PGP is the weekly safety net. Almost every registered longshoreman on the coast knows it exists. Far fewer can tell you how the weekly number is actually figured. And almost nobody is checking, on payday, whether the PGP line on their stub matches what they were really owed. That last part is the job DockBook does for you. But first, here is how the guarantee actually works.

What the PGP actually is

The Pay Guarantee Plan is a weekly earnings guarantee for registered longshoremen. If your earnings for a payroll week come in under a weekly cap, the PGP pays the difference, as long as you stayed eligible that week. It started in June 2024 under the current contract and runs every contract year.

The money behind it comes from PMA: $60 million the first year, $50 million each year after. That fund backs the weekly payments up and down the coast.

Your cap depends on your class:

- Class A: up to 40 hours a week guaranteed

- Class B with 5 or more vacation qualifying years: up to 40 hours a week

- Class B with fewer than 5: up to 32 hours a week

PGP hours are paid at your vacation skill rate, capped at Skill III. If you didn't earn vacation that year, the guarantee drops to the basic rate.

How the weekly math works

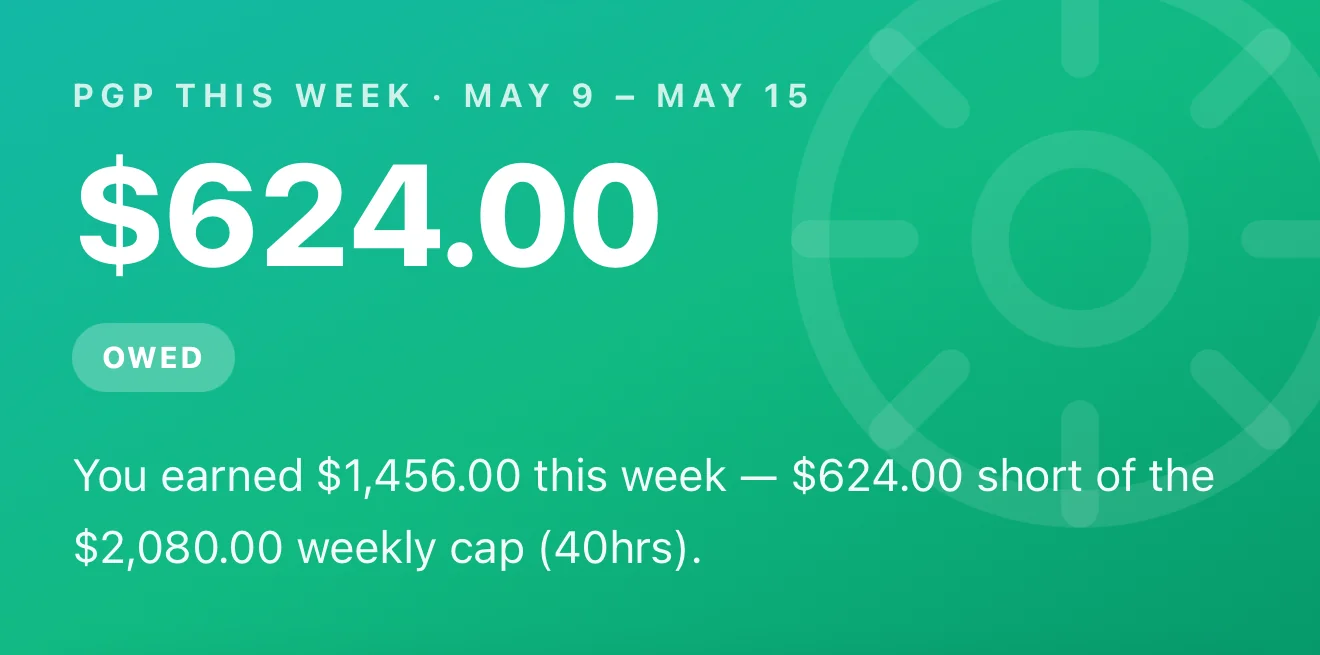

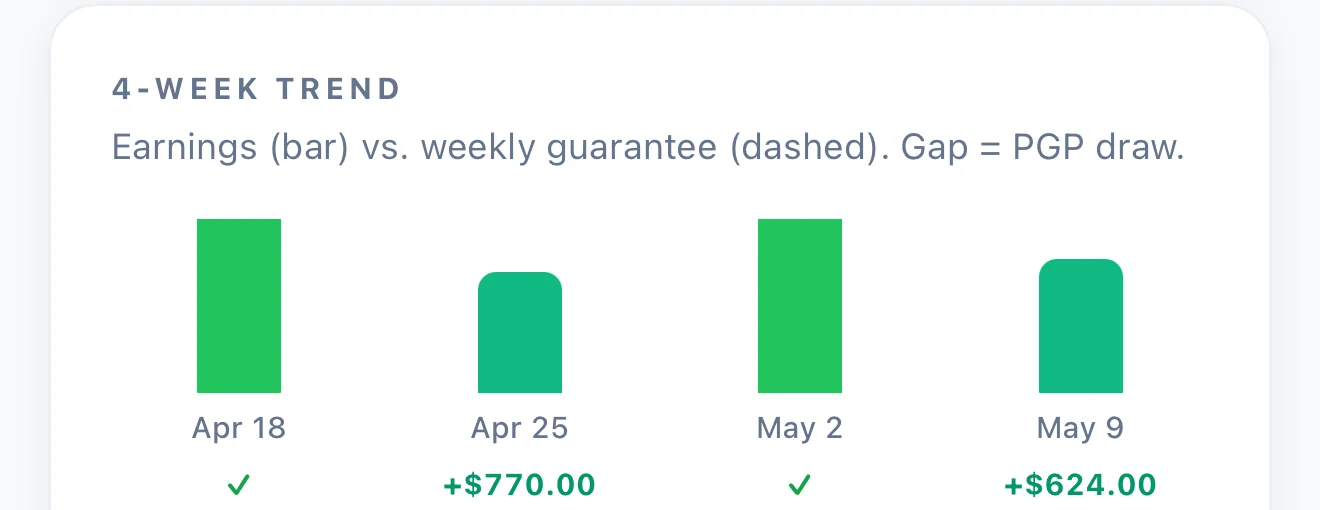

The mechanic is simple. Take your weekly cap. Subtract your gross longshore earnings for the payroll week. If there's a gap, the PGP fills it, paid in hours at your vacation skill rate. If you earned through the cap, PGP pays nothing that week.

Say you're Class A with a 40-hour cap. A short week (bad dispatch, weather, light cargo) leaves your gross at the equivalent of 22 hours. That's an 18-hour gap, and the PGP covers it.

One thing that surprises people: more than just straight-time counts against the cap. The contract also counts your overtime, skill pay, penalty cargo, travel pay, vacation and holiday pay, jury duty pay, State unemployment, even prior PGP payments and retirement income including Social Security. So if you're drawing State unemployment or a pension on the side, those dollars eat into the guarantee.

The Class B vacation-year ladder

This is the one that catches Class B guys off guard. Your cap is 32 hours until you stack up 5 vacation qualifying years, then it jumps to 40.

A vacation qualifying year isn't just "any year you worked." It's a year you earned at least one week of basic vacation, which runs around 552 hours coast-wide. Years where you fell short of that vacation floor don't move the ladder, even if you put in plenty of hours overall. And your very first year of registration doesn't count for PGP at all, so your registration clock and your ladder clock never quite line up.

The ladder, the port-by-port hour thresholds, and how to know where you stand all get their own breakdown in the Class B vacation-year ladder, explained.

What can cost you a PGP week

The contract has a handful of disqualifiers. Three worth knowing:

- Refusing a travel call. Travel between ports is required where it's customary or workable. Refuse a travel call when you're not on the travel-exempt list and you lose PGP for that week. The travel time and what you earn in the other port both still count toward your earnings record.

- Refusing clerk dispatch. Registered longshoremen get offered clerks' work ahead of casual clerks. Turn it down and you lose PGP for that week.

- Outside non-longshore income. Earn outside-source money during weekday shift hours, collect weekly indemnity, or fail to file for State unemployment when you should have, and you're disqualified. This one bites hardest: a violation can knock you out for the life of the contract or 12 months, whichever is longer.

These are easy to trip over and hard to keep straight. DockBook's PGP tracker flags this kind of risk as you log your week, so you catch "that was a travel-exempt call" or "that outside income landed on a weekday shift hour" before it costs you. The app flags it. PMA payroll still makes the final call, but you would rather see the risk coming than find it on your stub.

The eligible-weeks budget

PGP isn't unlimited. It's capped at 52 payroll weeks a year, minus any vacation weeks you were paid. Take four weeks of paid vacation and your PGP budget for the year is 48 weeks. Run out and it doesn't refill until the new contract year. That almost never bites, since most guys aren't on PGP every non-vacation week, but it's worth knowing if you're leaning on the guarantee through a thin stretch.

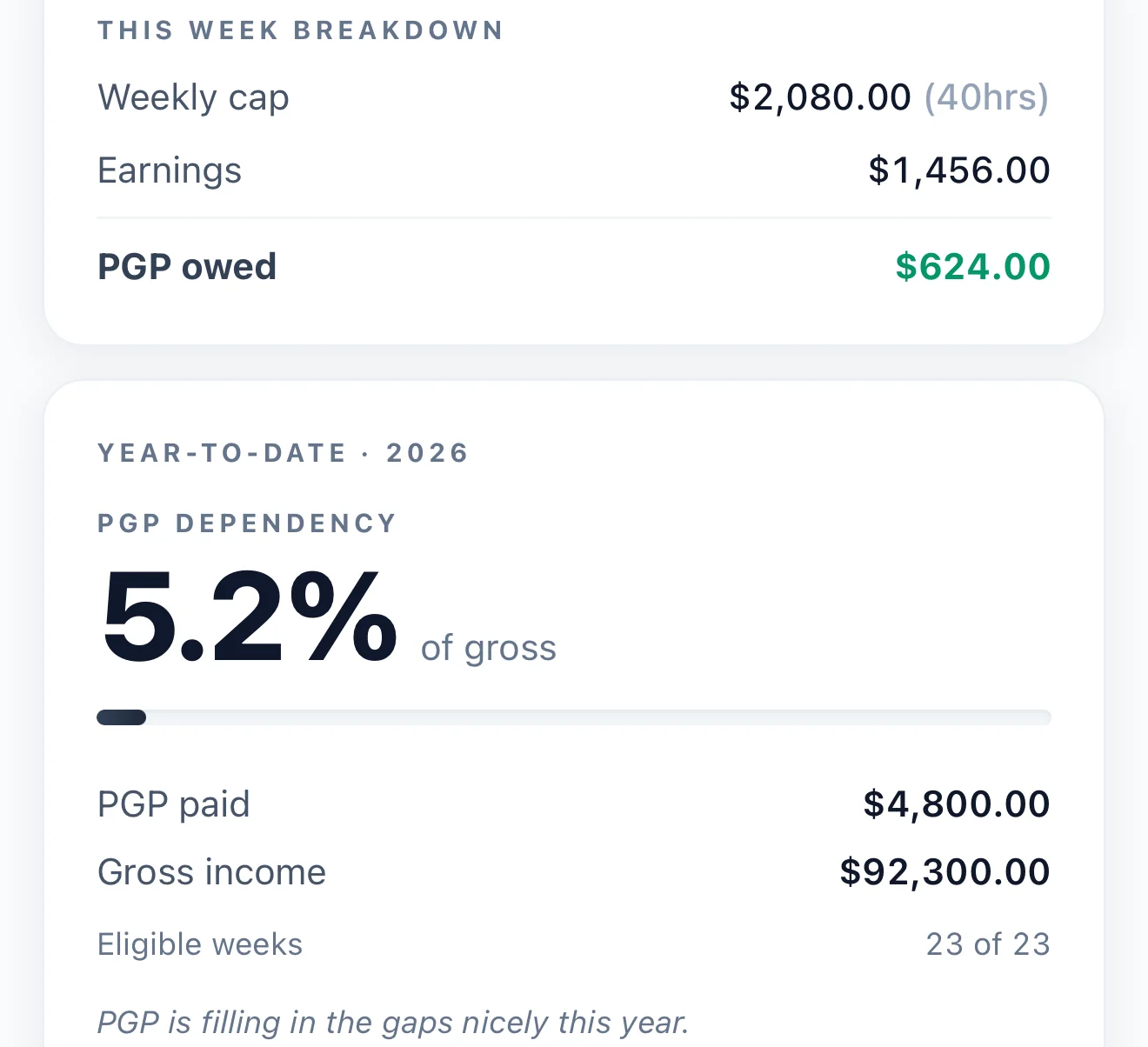

Why your dependency % matters

Dependency % is PGP paid divided by your total gross. It's the share of your income that came from the guarantee instead of from worked hours.

A small number is normal. Short weeks happen and the guarantee absorbs them. A high number is a signal: the work isn't there, your hall position isn't producing, or your dispatch pattern is leaving hours on the table. The PGP doesn't fix any of that. It papers over it.

The reason to watch the number is planning, not guilt. High dependency means thinner worked hours, and a PGP dollar doesn't build every benefit the way a worked hour does. Here is where that matters.

Where your PGP counts, and where it doesn't

This is the most-missed part of the whole guarantee: a PGP dollar doesn't count the same way in every plan. Two of your plans count it. One doesn't.

Your pension: it counts. A pension year of service is measured in hours. The pension plan spells out which hours count toward that year, and PGP is right there on the list, next to hours worked and vacation and holiday pay. Your PGP dollars convert to hours and move your pension forward.

Your health coverage: it counts here too. Welfare eligibility is earned in hours over a review period. The welfare plan credits your PGP toward that count, converted the same way: the PGP you were owed, divided by your straight-time rate. A slow stretch carried by PGP doesn't automatically cost your family its coverage.

Your 401(k): it doesn't count. The savings plan pays an employer contribution on your qualified hours, and qualified hours are the ones paid by employers plus your vacation and holiday pay. PGP is named on the "doesn't count" side, right next to disability pay. The employer contribution doesn't flow on a guarantee dollar.

There's a twist that cuts both ways. The 401(k) contribution only flows in a year if you qualified for a pension year of service the year before, and since PGP counts toward your pension, it can help you clear that gate. But once you're through it, the contribution is paid only on qualified hours, and PGP isn't one. PGP can get you in the door and earn you nothing once you're inside.

So in a PGP-heavy year, the 401(k) is the line to watch. Your pension and your health coverage both count the guarantee. The 401(k) is the one it leaves on the table. DockBook tracks your hours by type, so you can see your pace toward each one instead of finding out in July.

Checking your PGP each week

You can't audit a stub from the stub alone. You need your own record of what you worked to compare against. That's the whole reason the PGP tracker is in DockBook: log your shifts as you work them, punch in the PGP figure off your stub when it lands, and the app compares it to what the guarantee should have paid and flags the week that doesn't match. No envelope math, no eyeballing it.

When something is off, you walk into payroll with the specific week and the specific number, not a vague "I think I'm short." That is the difference between getting it fixed and getting nowhere.

The bottom line

PGP is your floor. Knowing the floor is the difference between hoping payroll got it right and knowing they did.

DockBook does the knowing for you. The PGP tracker, part of Pro, shows your weekly cap, your earnings, what you're owed, your dependency %, and checks each stub against the contract. If you're already logging your shifts, the PGP math falls out of what you've entered. See it on DockBook for PMA, or run a week right now on the free pay calculator.

A note on accuracy

This is a plain-English explainer based on the current longshore contract and the pension, welfare, and 401(k) plan documents. It's not a legal document, not financial advice, and not a substitute for the Plan office or a talk with your local. If your year is close to a threshold on any plan, confirm where you stand with the Plan office before you count on it.

Spot something out of date or wrong? Email me. I keep these updated as the contract changes.

Frequently asked

Does PGP count toward my pension?

Yes. A pension year of service is measured in hours, and PGP is on the list of hours that count, alongside worked hours, vacation, and holiday pay.

Does PGP count toward my 401(k)?

No. The 401(k) employer contribution is paid only on qualified hours, meaning employer-paid hours plus vacation and holiday pay. PGP is named on the side that does not count, next to disability pay.

What is the Class B weekly PGP cap?

32 hours a week until you reach 5 vacation qualifying years, then it steps up to 40. Class A is 40 hours.

What can disqualify me from PGP for a week?

Refusing a travel call when you are not on the travel-exempt list, refusing a clerk dispatch, or earning outside non-longshore income during weekday shift hours. PMA payroll determines actual disqualification.

How is the weekly PGP payment calculated?

Your weekly cap minus your gross longshore earnings for the week. If there is a gap, PGP fills it, paid in hours at your vacation skill rate, capped at Skill III.

Have a question about this post or spot something to fix? Email me directly.